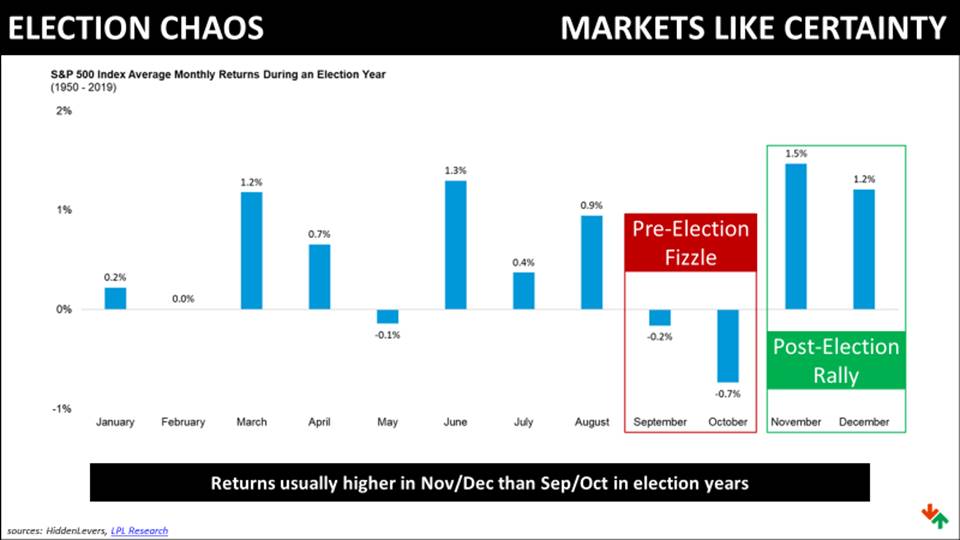

*Note: “Seasonality” refers to an old adage that the period from May through October has been a less reliable time of year for market growth

Market Recap: Earnings Resilience, Policy Tailwinds, and a Constructive Outlook

Lower expectations could set markets up for positive surprises

Earnings estimates for the second quarter of 2025 for the total S&P 500 (based on companies that have reported) are expected to be up +7.0% from the same period last year on +3.8% higher revenues. These earnings estimates have been lowered in a notable way, and many companies avoid providing earnings estimates altogether—which is rare but understandable in 2025’s version of “Trump 2.0”.

As of May 15, 2025, the S&P 500 has posted a modest year-to-date gain of 0.6%, recovering from earlier losses driven by tariff uncertainties. The Dow Jones Industrial Average and Nasdaq Composite remain slightly negative for the year. A significant rebound has been fueled by easing trade tensions and solid corporate earnings.

Tax Legislation: Potential Extensions and Business Incentives

In Washington, the House Ways and Means Committee has advanced a proposal to make permanent key provisions of the 2017 Tax Cuts and Jobs Act (TCJA), including the reduced corporate tax rate of 21%. The bill also introduces new deductions aimed at working-class taxpayers and extends pro-business measures like immediate expensing of capital investments. While the proposal faces debate, its advancement suggests potential continuity in a tax environment favorable to corporate profitability.

Trade Developments: U.S.-UK Agreement and Tariff Reductions

On the international front, the United States and the United Kingdom have signed a trade agreement that eliminates certain trade barriers and expands market access, creating a $5 billion opportunity for U.S. exporters. Additionally, a recent U.S.-China “agreement” has led to a significant reduction in tariffs, easing from an average of 24% to 14%, which has alleviated investor concerns over a potential trade war-induced recession. There are potential positive news flows from India and others in the coming weeks and months

Economic Indicators: Labor Market and Consumer Spending

Despite a -0.3% contraction in the first quarter 2025 GDP advance estimate, consumer spending grew by 1.8%, and business investment remained steady. The labor market continues to demonstrate strength, with an average of 155,000 jobs added per month over the past quarter and unemployment rates remaining low. These indicators suggest underlying economic resilience amid shifting expectations.

Looking Ahead

As we approach the mid-year mark, the combination of resilient corporate earnings, potential tax policy extensions, and favorable trade developments provides a constructive backdrop for the markets. While uncertainties remain, particularly regarding future earnings guidance and economic policies, the current environment offers opportunities for positive market performance in the latter half of 2025.

Still, our Reward-to-Risk analysis will guide us:

Patience, Discipline, Process, Customization.

Michael Hakerem

Chartered Financial Analyst

Chief Investment Officer

Advisory services offered through Kingswood Wealth Advisors, LLC an SEC Registered Investment Advisor, LLC. Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost. This content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.